Whether you’re in college or just entering the workforce, it is crucial to be responsible with your finances. However, it can be really scary and overwhelming to think about your money and the impact it has on your future. Here are three tips for managing your money!

1. Track your spending & Create a Budget

It is so easy to lose track of your spending. As a young adult, you should begin tracking your spending and creating a budget for yourself. This may seem intimidating, but it is actually really simple! Start by listing your monthly expenses in categories, such as bills, transportation, food, and entertainment. Access your spending and find things you can cut out of your spending on a monthly basis.

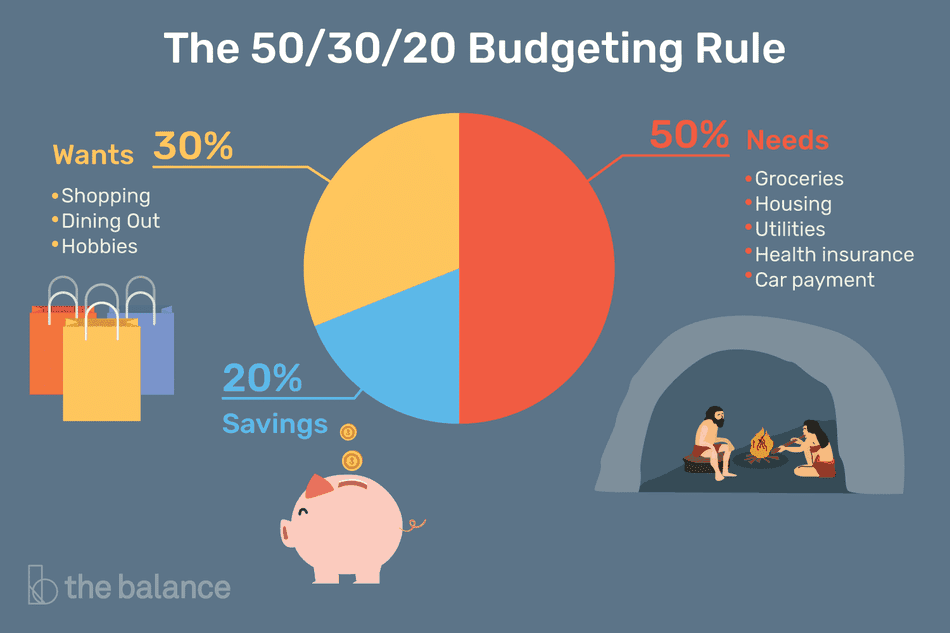

A simple and popular budgeting rule to follow is the 50-30-20 rule. This budgeting rule puts 50% of your monthly income toward necessities, such as rent and bills. 30% of your income goes towards “wants”, such as dining, shopping and entertainment. Finally 20% of your monthly income should go toward your savings.

There are also plenty of apps available that can help you create a budget and track your spending as well. Check out our blog about four personal finance apps here!

2. Build Your Credit

Credit cards can be very handy, as there are no overdraft fees. However, it is so important to only spend what you have and what you can pay back. Paying off your credit in full each month will help you build your credit up. A high credit score is very beneficial as it can help you in the future qualifying for loans and making big purchases.

Check out our blog about credit cards here for more information!

3. Start Saving Now

Using the 50-30-20 rule will make you put your money towards your savings, but even if you aren’t using that rule It is still important to start saving while you can, and building up.

It is a good idea to start an emergency fund. Putting money towards an emergency fund can help you tremendously down the road. Life can hit you by surprise. This emergency fund will be useful if any medical, vehicle or other unexpected expenses come up.

It is also important to save up as you start thinking about paying off your loans after graduating.

If you have a job, your employer may offer 401k benefits and you can start saving and investing!

In summary, track your spending, create a budget, build your credit, and start saving. These three simple tips will help you manage your money and make dealing with your finances much easier!

Edited by Marcus

Recent Comments